Compliance Recap | October 2023

October saw the release of adjusted civil penalties for HIPAA violations, ACA requirements, and Medicare Secondary Payer rules. Health plan limits and maximums for 2024 including high deductible health plans (HDHPs), health savings accounts (HSAs) flexible spending accounts (FSAs), and dependent care FSAs have been announced. Minnesota enacted a Paid Sick and Safe Leave Law to take effect on January 1, 2024, and California expanded its Paid Sick Leave. The IRS announced the annually adjusted Patient-Centered Outcomes Research Institute (PCORI) fee.

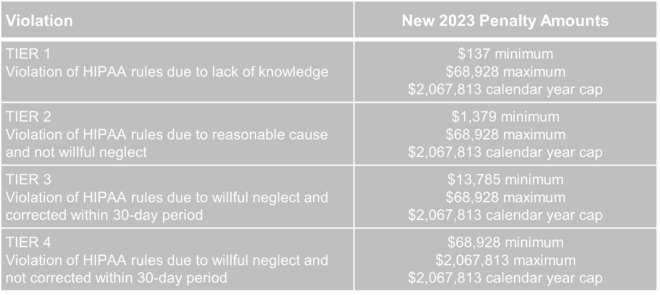

Adjusted Civil Penalties

The U.S. Department of Health and Human Services (HHS) has recently announced adjustments to civil penalties related to violations of the Health Insurance Portability and Accountability Act (HIPAA), the Affordable Care Act (ACA), and the Medicare Secondary Payer (MSP) rules. These penalty adjustments take into account inflation and are applicable to violations that occurred on or after November 2, 2015, and for which penalties are assessed on or after October 6, 2023.

HIPAA, which focuses on privacy and security rules, categorizes penalties based on the level of intention behind the violation.

The maximum penalty for failing to provide an SBC to eligible individuals before enrollment (or re-enrollment) in a group health plan has increased from $1,264 to $1,362.

The Medicare Secondary Payer (MSP) rules prevent employers from providing incentives to Medicare beneficiaries to waive or terminate primary group health plan coverage. The maximum penalty for not complying with MSP rules has increased to $11,162 from $10,360. Furthermore, the maximum penalty for failing to inform HHS when a group health plan is or was primary to Medicare has risen to $1,428 from $1,325.

Employer Considerations

To avoid these penalties, employers should carefully review their plan documents and operations to ensure compliance with the HHS-related requirements.

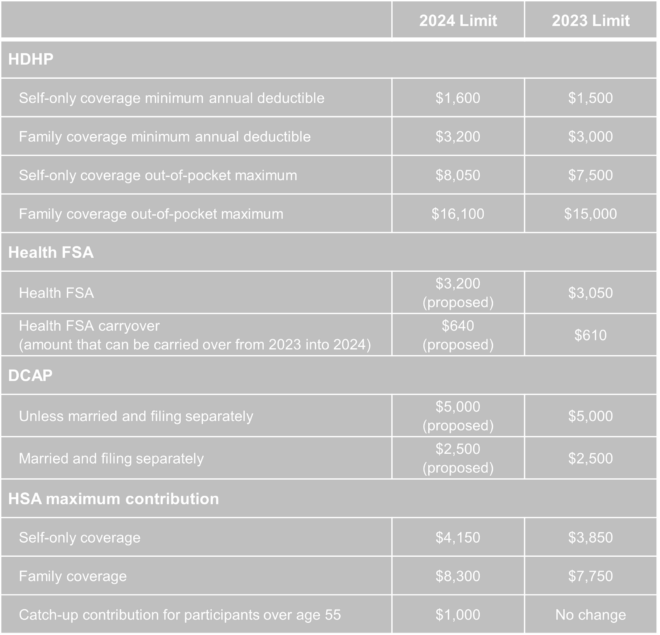

2024 Limits Announced for HDHPs, HSAs, FSAs

The Internal Revenue Service (IRS) announced the new limits for high-deductible health plans (HDHPs), health savings accounts (HSAs), and Dependent Care Assistance Plans (DCAPs), and health flexible spending arrangements (FSAs). The new limits take effect beginning January 1, 2024.

Minnesota Paid Sick and Safe Leave Law

Minnesota has recently passed a statewide paid sick and safe time leave law set to take effect on January 1, 2024. This law mirrors similar laws already in place in four Minnesota cities—Minneapolis, St. Paul, Duluth, and Bloomington. The key feature of the state law is the “front loading method,” which allows employers to provide employees with 48 hours of earned sick and safe time (ESST) in the first year of employment. Employers can pay out the value of unused hours at the end of the year and avoid carrying over unused hours into the next year.

Employer Considerations

This option provides flexibility for employers in managing employee leaves of absence. Local ordinances are not preempted by the state law, and employers must follow the most protective provisions of the state or local ordinances. The determination of which is more protective depends on whether more leave or monetary benefits are considered more beneficial for employees. See the FAQs for more information.

California Expands Paid Sick Leave

On October 4, 2023, Governor Gavin Newsom signed Senate Bill No. 616 into law, amending California’s paid sick leave regulations. The key changes introduced by SB 616 are:

- Starting January 1, 2024, California employers must provide employees with five days or 40 hours of paid sick leave, an increase from the previous requirement of three days or 24 hours.

- Employers can continue to provide paid sick leave at a rate of one hour for every 30 hours worked. If they use a different accrual rate, employees must accrue a minimum of 40 hours by their 200th day of employment and at least 24 hours by the 120th day of employment. Employers can also front load the entire paid sick leave amount.

- Employers may still limit the annual use of paid sick leave, but SB 616 increases the annual usage cap from 24 hours to 40 hours. The bill allows employers to cap paid sick leave accrual at 80 hours or 10 days, up from the previous limit of 48 hours or six days.

- While SB 616 continues to exempt certain collective bargaining agreement employees from the accrual requirement, it extends some provisions of California’s paid sick leave law to non-construction industry collective bargaining agreement employees. These employees may use paid sick leave for specific reasons, such as health-related issues or domestic violence, without facing retaliation. Employers cannot require these employees to find replacement workers when using sick days.

Employer Considerations

To comply with SB 616, employers are advised to review and update their paid sick leave policies to align with the new requirements and usage caps. Human resources and managers should also ensure proper implementation and adherence to the law.

Adjusted PCORI Fee

The IRS has announced an annual increase in Patient-Centered Outcomes Research Institute (PCORI) fees, which are required to be paid by health insurers and self-insured health plan sponsors. PCORI fees were established by the Affordable Care Act (ACA) to fund clinical effectiveness research.

The PCORI fee amount is adjusted each year based on the percentage increase in projected per capita national health expenditures. For plan and policy years ending on or after October 1, 2023, and before October 1, 2024, the adjusted applicable dollar amount will be $3.22, marking a $0.22 increase from the previous year. To calculate PCORI fees, multiply the applicable dollar amount by the average number of covered lives in the plan or policy.

Employer Considerations

These fees must be paid annually using IRS Form 720 no later than July 31 of the calendar year immediately following the last day of the relevant policy or plan year. Insurers, plan sponsors, and their advisors should ensure they have this date marked on their compliance calendars.

Question of the Month

- My wife and I work in the same small company. Is having her on my plan as spouse allowed? Can we both contribute separately from our own paychecks into our own Health Savings Account (HSA)? Or does it need to be my deduction only since I am the policy holder?

- Yes, each spouse can have an HSA. The family limit, however, is divided between the two spouses, meaning the contributions to both HSAs combined cannot exceed the family HSA contribution limit.