Nondiscrimination Rules for Cafeteria Plans

Updated January 2020

A cafeteria plan is an employer-provided written plan that offers employees the opportunity to choose between at least one permitted taxable benefit and at least one qualified employee benefit. There is no federal law that requires employers to establish cafeteria plans; however, some states require employers to have cafeteria plans for employees to pay for health insurance on a pre-tax basis.

To comply with Internal Revenue Code Section 125, a cafeteria plan must satisfy a set of structural requirements and a set of nondiscrimination rules. Violations of the structural requirements will disqualify the entire plan so that no employee obtains the favorable tax benefits under Section 125, even if the plan meets the nondiscrimination rules. Violations of the nondiscrimination rules have adverse consequences only on the group of employees in whose favor discrimination is prohibited.

A cafeteria plan must pass an eligibility test, a contributions and benefits test, and a concentration test for highly compensated individuals to receive the tax benefits of Section 125. Failure to meet these nondiscrimination requirements has no effect on non-highly compensated cafeteria plan participants.

The IRS issued proposed cafeteria plan regulations on August 6, 2007. Final regulations have not been issued. According to the proposed regulations, taxpayers may rely on the proposed regulations for guidance pending the issuance of final regulations.

The proposed cafeteria plan regulations make it clear that the plan must meet the nondiscrimination tests. Also, the plan must not discriminate in favor of highly compensated participants in its operation. For example, a plan might be considered discriminatory if adoption assistance is added to the plan when the CEO is in the process of adopting a child and adoption assistance is dropped when the adoption is final.

Be aware that Section 125 nondiscrimination rules are separate from and unrelated to Section 105(h) nondiscrimination rules. Further, Section 125 nondiscrimination rules apply to all cafeteria plans regardless of their status as fully insured, self-funded, church plan, or governmental plan.

As a practical matter, these nondiscrimination rules prohibit executive health plans offered through a cafeteria plan.

Nondiscrimination Testing

Definitions

There are a number of definitions of key terms used in the tests that must be understood prior to completing the tests.

- Highly Compensated Individuals. Highly compensated individuals are defined as:

- Officers

- 5 percent shareholders

- Highly compensated employees (HCEs)

- Spouses or dependents of any of the preceding individuals

- Highly Compensated Participant. A highly compensated participant is a highly compensated individual who is eligible to participate in the cafeteria plan.

- Officers. Officers include any individual who was an officer of the company for the prior plan year (or current plan year in the case of the first year of employment).

- Five Percent Shareholders. Five percent shareholders include any individual who – in either the preceding plan year or current plan year – owns more than 5 percent of the voting power or value of all classes of stock of the employer, determined without attribution.

- Highly Compensated. Highly compensated means any individual or participant who – for the prior plan year or the current plan year in the case of the first year of employment – had annual compensation from the employer in excess of the compensation amount specified in the Internal Revenue Code and, if elected by the employer, was also in the top-paid group of employees for the year. For 2018, the applicable compensation amount is $120,000. For 2019, the applicable compensation amount is $125,000.

- Key Employee. A key employee is a participant who, at any time during the plan year, is one of the following:

-

- An officer with annual compensation greater than an indexed amount ($175,000 for 2018, $180,000 for 2019, $185,000 for 2020)

- A five percent owner of the employer

- A one percent owner having compensation in excess of $150,000

Eligibility Test

A Section 125 cafeteria plan cannot discriminate in favor of highly compensated individuals as to eligibility to participate in the plan.

A plan’s eligibility requirements do not favor highly compensated individuals if the plan satisfies the following safe harbor criteria:

- It meets the nondiscriminatory classification test contained in Code Section 410(b)(2)(A)(i), a section that deals with minimum coverage requirements for qualified retirement plans;

- It does not require more than three years of service as a precondition for participation;

- It imposes a uniform minimum service requirement for all employees; and

- Employees who satisfy the uniform participation requirement start plan participation no later than the first day of the first plan year beginning after the condition is satisfied.

For number one above, a cafeteria plan does not discriminate in favor of highly compensated individuals if the plan benefits a group of employees who qualify under a reasonable classification established by the employer (which is defined by the Internal Revenue Code) and the group of employees included in the classification satisfies either the safe harbor percentage test or an unsafe harbor percentage component of the facts and circumstances test.

An employer’s classification of employees is reasonable if, based on all the facts and circumstances, the classification is established under objective business criteria that identify the category of employees who benefit under the plan. Reasonable classifications generally include specified job categories, nature of compensation (that is, salaried or hourly), geographic location, and similar bona fide business criteria.

Below is information on how to determine the safe harbor percentage or the unsafe harbor percentage component of the facts and circumstances test.

To apply the percentage tests, the percentage of non-highly compensated individuals who benefit under the plan is divided by the percentage of highly compensated individuals who benefit. The non-highly compensated individual concentration percentage of an employer is the percentage of all the employees of the employer who are non-highly compensated individuals.

Generally speaking, the plan may exclude the following employees for purposes of the safe harbor percentage test and the unsafe harbor percentage component of the facts and circumstances test, so long as the individual is not participating in the plan:

- Employees with fewer than three years of service

- Employees participating in the cafeteria plan under a COBRA continuation provision

- Employees covered by a collective bargaining agreement

- Non-resident aliens with no U.S. source of income

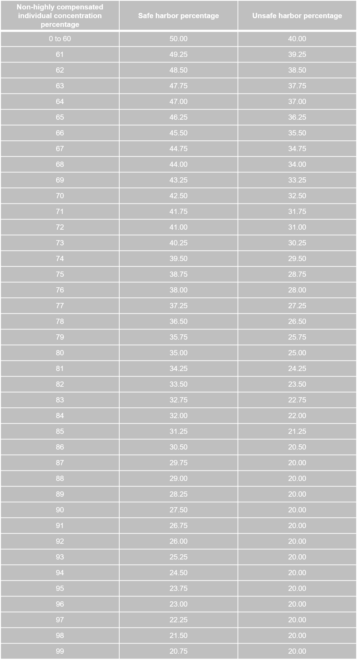

The exact ratio for a particular employer to meet the tests depends on the concentration of non-highly compensated individuals in the plan. Acceptable ratios range from 50 percent to 20 percent.

The safe harbor percentage of an employer is 50 percent, reduced by 3/4 of a percentage point for each whole percentage point by which the non-highly compensated individual concentration percentage exceeds 60 percent.

The unsafe harbor percentage of an employer is 40 percent, reduced by 3/4 of a percentage point for each whole percentage point by which the non-highly compensated individual concentration percentage exceeds 60 percent. However, in no case is the unsafe harbor percentage less than 20 percent.

The following table sets forth the safe harbor and unsafe harbor percentages at each non-highly compensated individual concentration percentage.

If the plan has neither passed the safe harbor test nor failed the unsafe harbor test, it may be considered nondiscriminatory based on a review of all facts and circumstances, including the following:

- The underlying business reason for the classification.

- The percentage of employees benefiting under the plan.

- Whether the number of employees benefiting under the plan in each salary range is representative of the total number of employees in that salary range.

- The difference between the plan’s ratio percentage and the employer’s safe harbor percentage.

- The extent to which the plan’s average benefit percentage exceeds 70 percent.

Below are examples from the regulations that illustrate the rules regarding nondiscriminatory classification.

- Example 1: Employer A has 200 non-excludable employees, of whom 120 are non-highly compensated employees and 80 are highly compensated employees. Employer A maintains a plan that benefits 60 non-highly compensated employees and 72 highly compensated employees. Thus, the plan’s ratio percentage is 55.56 percent ([60/120] / [72/80] = 50%/90% = 0.5556), which is below the percentage necessary to satisfy the ratio percentage test of § 1.410(b)-2(b)(2). The employer’s non-highly compensated employee concentration percentage is 60 percent (120/200); thus, Employer A’s safe harbor percentage is 50 percent and its unsafe harbor percentage is 40 percent. Because the plan’s ratio percentage is greater than the safe harbor percentage, the plan’s classification satisfies the safe harbor . . . of this section.

- Example 2: The facts are the same as in Example 1, except that the plan benefits only 40 non-highly compensated employees. The plan’s ratio percentage is thus 37.03 percent ([40/120] / [72/80] = 33.33%/90% = 0.3703). Under these facts, the plan’s classification is below the unsafe harbor percentage and is thus considered discriminatory.

- Example 3: The facts are the same as in Example 1, except that the plan benefits 45 non-highly compensated employees. The plan’s ratio percentage is thus 41.67 percent ([45/120] / [72/80] = 37.50%/90% = 0.4167), above the unsafe harbor percentage (40 percent) and below the safe harbor percentage (50 percent). The Commissioner may determine that the classification is nondiscriminatory after considering all the relevant facts and circumstances.

- Example 4: Employer B has 10,000 non-excludable employees, of whom 9,600 are non-highly compensated employees and 400 are highly compensated employees. Employer B maintains a plan that benefits 600 non-highly compensated employees and 100 highly compensated employees. Thus, the plan’s ratio percentage is 25.00 percent ([600/9,600] / [100/400] = 6.25%/25% = 0.2500), which is below the percentage necessary to satisfy the ratio percentage test of § 1.410(b)-2(b)(2). Employer B’s non-highly compensated employee concentration percentage is 96 percent (9,600/10,000); thus, Employer B’s safe harbor percentage is 23 percent, and its unsafe harbor percentage is 20 percent. Because the plan’s ratio percentage (25.00 percent) is greater than the safe harbor percentage (23.00 percent), the plan’s classification satisfies the safe harbor of paragraph (c)(2) of this section.

- Example 5: The facts are the same as in Example 4, except that the plan benefits only 400 non-highly compensated employees. The plan’s ratio percentage is thus 16.67 percent ([400/9,600] / [100/400] = 4.17%/25% = 0.1667). The plan’s ratio percentage is below the unsafe harbor percentage and thus the classification is considered discriminatory.

- Example 6: The facts are the same as in Example 4, except that the plan benefits 500 non-highly compensated employees. The plan’s ratio percentage is thus 20.83 percent ([500/9,600] / [100/400] = 5.21%/25% = 0.2083), above the unsafe harbor percentage (20 percent) and below the safe harbor percentage (23 percent). The Commissioner may determine that the classification is nondiscriminatory after considering all the facts and circumstances.

Contributions and Benefits Test

A Section 125 cafeteria plan cannot discriminate in favor of highly compensated participants with regard to contributions and benefits. A cafeteria plan must satisfy this component with respect to both benefit availability and benefit utilization.

This means that a cafeteria plan must give each similarly situated participant a uniform opportunity to elect qualified benefits; further, highly compensated participants must not disproportionately elect qualified benefits.

Qualified benefits are disproportionately elected by highly compensated participants if the total qualified benefits elected by highly compensated participants (measured as a percentage of the total compensation of highly compensated participants) are more than the total qualified benefits elected by non-highly compensated participants (measured as a percentage of the total compensation of non-highly compensated participants).

Plan passes benefits test if:

Employer contributions are disproportionately utilized by highly compensated participants if the aggregate contributions utilized by highly compensated participants, measured as a percentage of aggregate compensation of highly compensated participants, exceed the aggregate contributions utilized by non-highly compensated participants measured as a percentage of the aggregate compensation of non-highly compensated participants.

Plan passes contributions test if:

Nondiscriminatory 25% Concentration Test

If a Section 125 cafeteria plan provides more than 25 percent of its nontaxable benefits (excluding group term life insurance in excess of $50,000) to key employees, then each key employee includes in gross income an amount equaling the maximum taxable benefits that he or she could have elected for the plan year.

Safe Harbors for Cafeteria Plans

Health Plan Safe Harbor

This health plan safe harbor applies only to cafeteria plans that provide health benefits. Under the health plan safe harbor, the definition of health benefits is limited to major medical coverage; it excludes dental coverage or health care flexible spending accounts (FSAs).

Health benefits will be treated as nondiscriminatory under the health plan safe harbor if:

- Contributions on behalf of each participant equal either:

- 100 percent of the cost of coverage of the majority of similarly situated highly compensated participants, or

- at least 75 percent of the cost of coverage of the similarly situated participants having the highest cost health benefit under the plan; and

- Contributions or benefits that exceed those described in #1 above bear a uniform relationship to compensation.

Safe Harbor Test for Premium-Only Plans

The proposed regulations include a safe harbor for premium-only plans. A premium-only plan is a cafeteria plan that offers as its only benefit an election between cash and the payment of the employee share of the premium for employer-provided health insurance.

Under this safe harbor, a premium-only plan satisfies the cafeteria plan nondiscrimination requirements if it satisfies the safe harbor percentage test for eligibility (described earlier), regardless of the actual benefits chosen by employees. In other words, the plan will automatically satisfy the contributions and benefits test and the key employee concentration test for that plan year if the plan passes the eligibility test for that plan year.

SIMPLE Cafeteria Plan

Under the Patient Protection and Affordable Care Act (ACA), a SIMPLE cafeteria plan is a safe harbor plan that will automatically satisfy the overall cafeteria plan nondiscrimination rules as well as the nondiscrimination rules that apply separately to certain specified qualified benefits provided under the plan.

An employer qualifies to establish a SIMPLE cafeteria plan for a plan year if the employer employed an average of 100 or fewer employees on business days during either of the two preceding years. An employer may establish a SIMPLE cafeteria plan for a plan year beginning after December 31, 2010.

Once an employer qualifies as an eligible small employer and maintains a SIMPLE cafeteria plan for any year, the employer can continue to maintain a SIMPLE cafeteria plan for employees (including new employees) of the same trade or business until the year after it employs an average of 200 or more employees in a particular year.

A SIMPLE cafeteria plan must meet two requirements:

- A minimum eligibility and participation requirement; and

- A minimum contribution requirement.

Minimum Eligibility and Participation Requirement

An employer satisfies the minimum eligibility and participation requirement if:

- All employees with at least 1,000 hours of service for the preceding plan year are eligible to participate; and

- Each employee eligible to participate may elect any benefit available under the plan (subject to terms and conditions that apply to all participants).

A SIMPLE cafeteria plan may exclude employees who:

- Have not reached 21 years of age before the close of the plan year.

- Have not completed one year of service with the employer as of any day during the plan year.

- Are covered under a collective bargaining agreement in which benefits provided by the cafeteria plan were the subject of good faith bargaining between employee representatives and the employer.

- Are nonresident aliens working outside of the U.S.

Minimum Contribution Requirement

To qualify as a SIMPLE cafeteria plan, the plan must require the employer to make a minimum contribution to provide benefits under the plan on behalf of each qualified employee, whether or not the employee makes salary reduction contributions to the plan.

For purposes of the minimum contribution requirement rule, the following definitions apply:

- Qualified employee. A qualified employee is any employee who is not a highly compensated employee or a key employee.

- Highly Compensated Employee. A highly compensated employee is an employee who:

- Was a 5 percent owner at any time during the year or the preceding year; or

- For the preceding year, received compensation from the employer in excess of an indexed amount ($120,000 in 2018, $125,000 in 2019) and, if the employer elects, was in the top-paid 20 percent of employees for the preceding year.

- Key Employee. A key employee is any individual who, at any time during the plan year or any of the prior four years, is one of the following:

- An officer with annual compensation greater than an indexed amount ($175,000 for 2018, $180,000 for 2019, $185,000 for 2020)

- A five percent owner of the employer

- A one percent owner having compensation in excess of $150,000

- Minimum Contribution. The minimum contribution may be calculated under one of two methods: the non-elective contribution method or the matching contribution method. The same method must be used for all qualified employees.

- Non-elective Contribution Method: The minimum contribution on behalf of each qualified employee must equal a uniform percentage (not less than 2 percent) of the eligible employee’s compensation for the plan year, determined without regard to whether the employee makes any salary reduction contribution under the cafeteria plan.

- Matching Contribution Method. The minimum matching contribution is the lesser of:

- 100 percent of the amount of the salary reduction contributions elected to be made by the qualified employee for the plan year; or

- 6 percent of the qualified employee’s compensation for the plan year.

A SIMPLE cafeteria plan can provide matching contributions in addition to the minimum required contributions, but only if matching contributions with respect to salary reduction contributions for any highly compensated employee or key employee are not made at a greater rate than matching contributions for any non-highly compensated employee. An employer may provide qualified benefits under the plan in addition to required contributions.

A plan that satisfies the two requirements above – the minimum eligibility and participation requirement, and the minimum contribution requirement – for the plan year will be treated as meeting the following applicable nondiscrimination requirements for the year:

- The cafeteria plan nondiscrimination requirements in Section 125(b).

- The nondiscrimination requirements for employer-provided group term life insurance in Section 79(d).

- The nondiscrimination requirements for dependent care assistance programs under Section 129(d).

- The health benefit nondiscrimination requirements in Section 105(h).

Testing Frequency

Nondiscrimination testing must occur as of the last day of the plan year, taking into account all non-excludable employees (or former employees) who were employees on any day during the plan year.

As a best practice, an employer should test three times a year (for example, before the beginning of the plan year, several months before the end of the plan year, and after the close of the year) to take corrective action if it appears that the plan will not pass testing. Be aware that Section 125 plan corrections cannot be made after the plan year.

Conclusion

As a practical matter, the IRS has not recently focused on cafeteria plan nondiscrimination testing. However, if the IRS audits an employer, then the employer will need to furnish the results of the required testing and documentation of the employer’s corrective actions in response to any failed tests.

Be aware that a plan will not be treated as satisfying the nondiscrimination testing requirements if there are repeated changes to plan testing procedures or plan provisions that have the effect of manipulating the nondiscrimination testing results.

As a reminder, if the plan violates one of the structural requirements of Section 125, then the plan will not be a valid cafeteria plan and no participant will be entitled to favorable tax treatment under Section 125. If the plan fails to satisfy the structural requirements of Section 125 or fails to operate according to its written plan, then each employee’s election between taxable and nontaxable benefits results in gross income to the employee.

In contrast, a highly compensated participant or key employee in a discriminatory cafeteria plan must include in gross income the value of the taxable benefit with the greatest value that the employee could have elected to receive, even if the employee elects to receive only the nontaxable benefits offered. This requires both the employer and the affected employees to amend past tax filings to account for undeclared gross income, unpaid Social Security, FICA, FUCA and more.

There are no adverse tax consequences for non-highly compensated participants in a discriminatory cafeteria plan.

8/25/2016

Updated 5/30/2018

Updated 11/19/2018

Updated 1/31/2020